From 176 papers in 2013 to 20,668 in 2025, there is a 117x increase in twelve years. Blockchain research has evolved through three distinct eras. A Bitcoin-only genesis (2013 to 2016), an Ethereum-driven explosion (2017 to 2019), and a maturing institutional phase (2020 to present) where annual output now exceeds 20,000 papers. Across 128,286 concept-tagged publications indexed by OpenAlex through mid-2026, the data reveals a field that has decisively shifted from speculative experimentation to deployment-ready infrastructure, with post-quantum cryptography, regulatory compliance, and AI convergence emerging as the dominant research frontiers.

I. Methodology

This analysis draws on a primary corpus of 128,286 academic papers tagged as blockchain (C2779687700) or cryptocurrency (C180706569) by OpenAlex's machine-learning concept classifier, published between 2013 and mid-2026. Unlike title-only keyword searches that systematically undercount papers, the concept tagger evaluates full abstracts, citation networks, and contextual metadata, capturing papers like "Privacy-Preserving Data Sharing for Healthcare Systems" that use blockchain methods without placing "blockchain" in the title.

The corpus was cross-validated against four independent databases. These are Crossref (124,333 papers), Europe PMC (61,191), arXiv (11,312), and DBLP (37,246). The Crossref count closely matches the primary corpus, providing independent confirmation of coverage. Journal articles dominate at 68.9%, followed by book chapters (13.9%) and preprints (8.2%). Approximately half (50.2%) of the concept-tagged corpus is published as open access, making it highly accessible compared to standard academic baselines. A full n-gram frequency analysis (unigrams, bigrams, and trigrams) was executed across all paper abstracts to isolate the specific technical implementations and research domains commanding the field's attention.

II. The Research Map

Publication Volume & Milestone Timeline Track the 117x growth trajectory from Bitcoin-era genesis to institutional-era maturation.

Publication Volume & Milestone Timeline (2013 to 2026)

Publication volume and key milestones from genesis to maturationDocuments

18,800

Avg Citations

0.1

Milestone Context

On pace for ~18,800. Quantum-resistant and AI convergence accelerate.

As research volume surged 117x, the average citations per paper decayed from 85.0 to 0.1 due to Recency Effect and volume diluting attention.

The keyword analysis across the full corpus exposes a clear hierarchy of research priorities. "Blockchain" appears in 68.5% of all abstracts (87,818 papers), the universal anchor term. "Security" ranks third at 46.3% (59,388 papers), confirming that trust and tamper-resistance remain central to blockchain's value proposition. Nearly half of all blockchain papers discuss security in their abstracts.

The critical signal is that "smart contract" (29.9%) has overtaken "bitcoin" (27.9%) in abstract frequency. The field's center of gravity has moved from cryptocurrency mechanics to programmable execution layers. "Supply chain" (19.3%), "healthcare" (13.7%), and "energy" (16.0%) reflect blockchain's expansion into applied domains.

Linguistic N-Gram Corpus Frequency Analyzer Toggle between unigrams, bigrams, and trigrams to analyze which concepts dominate 128,286 paper abstracts.

Linguistic N-Gram Frequency Analyzer

Token frequency distribution across 128,286 abstracts“blockchain technology”

Dominant bigram: blockchain treated as modular infrastructure component.

Five structural findings define the current research map.

- Infrastructure Integration, Not Standalone Products. "Blockchain technology" (44,102 mentions) and "blockchain based" (18,516) dominate bigrams. Researchers treat blockchain as a modular component (an immutable audit layer, a state synchronization engine) within broader enterprise systems, not a monolithic replacement.

- Smart Contract Maturation. "Smart contract" appears in 21,134 bigram mentions and 38,414 unigram mentions (29.9% of abstracts). The research focus has shifted from conceptual design to formal verification, vulnerability auditing, and production-grade deployment.

- Supply Chain Dominance. "Supply chain" (11,418 bigram mentions) remains the single largest non-financial application vertical. Global logistics and manufacturing consortiums continue to build blockchain-based provenance, anti-counterfeiting, and multi-party transparency systems.

- The Blockchain-AI Convergence. "Machine learning" (5,667) and "artificial intelligence" (5,463) together account for 11,130 combined mentions, the largest technology convergence in the corpus. Papers apply AI to blockchain problems (anomaly detection, MEV optimization) and use blockchain for AI governance (decentralized model training, data provenance).

The Blockchain-AI Convergence Architecture

Decentralized coordination layers connecting artificial intelligence with cryptographyStrategic Rationale

Blockchain coordinates decentralized AI training across multiple nodes. It manages parameter updates, calculates model accuracy rewards, and prevents malicious model poisoning—all without centralizing raw training data.

Exemplar Research Document

“Blockchain empowered asynchronous federated learning for secure data sharing”- Sovereign Digital Currencies. "Central bank digital" (867 trigram mentions) and "bank digital currency" (864) reflect the institutional pivot toward CBDC infrastructure, with CBDC research growing from 1 paper in 2016 to 205 in 2025 as central banks deploy pilot programs globally.

Method Lifecycles

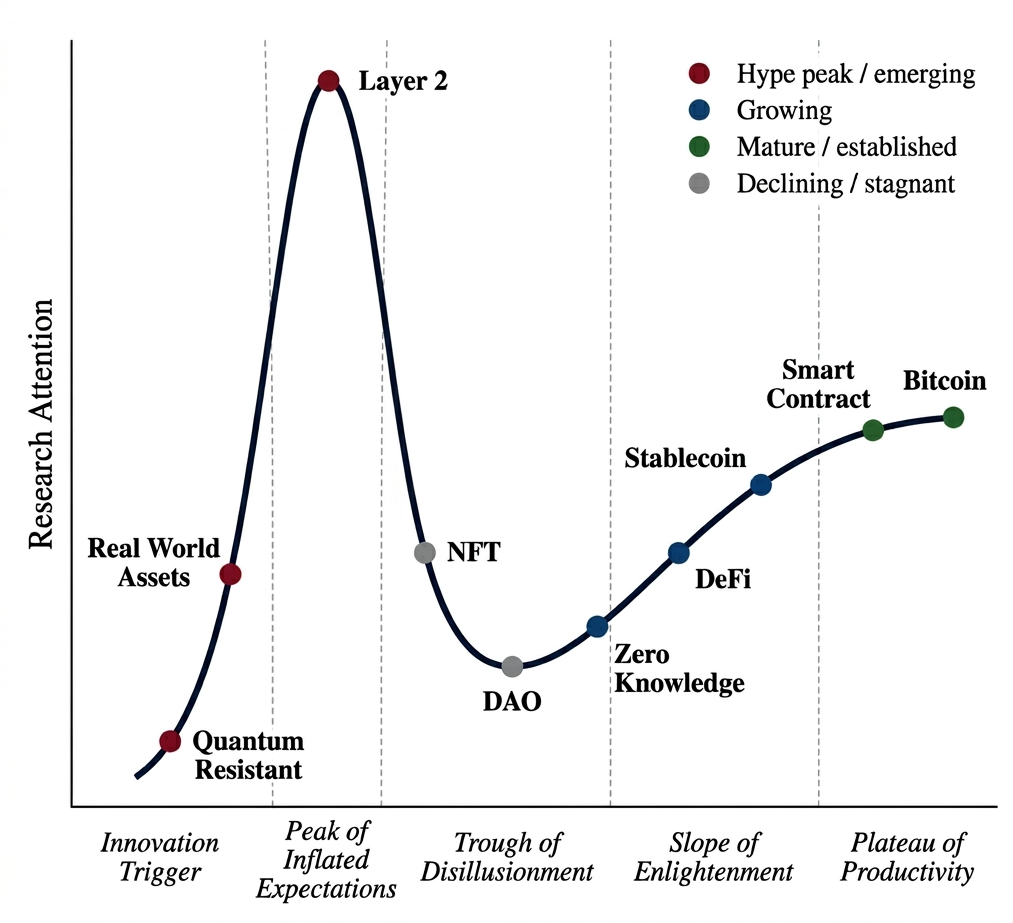

To trace the development of different blockchain technologies, we map the relative growth and maturity of key terms onto an interpretive research Hype Cycle.

- Innovation trigger and ascending hype. Emerging topics such as "quantum resistant" and "real world asset" occupy the Innovation Trigger phase due to high growth ratios off small baselines.

- Peak of inflated expectations. Scalability infrastructure like "layer 2" and "zk rollup" are located near the Peak of Inflated Expectations, alongside "regulatory" frameworks.

- Trough of disillusionment. "NFT" and "metaverse" research sit in the Trough of Disillusionment, following a contraction in paper volume.

- Slope of enlightenment. Core DeFi concepts and interoperability protocols are positioned in the Slope of Enlightenment.

- Plateau of productivity. Foundational elements like "smart contract", "consensus", and "supply chain" are in the Plateau of Productivity.

III. Three Eras of Blockchain Research

The publication volume data reveals three distinct phases in blockchain's academic trajectory.

The Bitcoin Era (2013 to 2016). Annual output grew from 176 to 955 papers. Research focused on cryptocurrency mechanics, mining economics, and Bitcoin transaction analysis. The total output of 2,111 papers over four years is smaller than a single month of 2025 output.

The Smart Contract Era (2017 to 2019). Growth was fastest at +163.9% in 2017 and +177.6% in 2018, the highest YoY expansion in the corpus. Ethereum's smart contract platform and the 2017 ICO boom generated massive academic interest. Annual output increased 11x from 955 (2016) to 10,591 (2019) in three years.

The Institutional Era (2020 to present). Growth decelerated to sustainable rates as the field matured. The 2024 growth of +1.8% represents the lowest annual increase in the corpus. Research pivoted to deployment challenges like scalability (layer 2, zero-knowledge proofs), regulation (3.5x growth), institutional finance (stablecoins, real-world assets, CBDCs), and post-quantum security. Papers published from 2020 onward account for 82.7% of the corpus. More than four in five blockchain papers were published in the last six years.

IV. The DeFi-NFT Divergence

DeFi and NFTs followed sharply different research trajectories, and the divergence is instructive.

DeFi research continues to accelerate. From near-zero papers before 2019 (7 papers), mentions grew to 12 in 2020, 63 in 2021, and 516 in 2025, a 74x increase over six years. The 2025 count exceeds all prior years. The annualized 2026 estimate (~584 papers) suggests continued acceleration. DeFi addresses a persistent structural problem (financial intermediation) with measurable efficiency gains.

NFT research has peaked and declined. NFT mentions grew to 60 in 2021, peaked at 426 in 2023, then fell to 334 in 2024. The 2023 peak coincides with the collapse of NFT trading volumes. A modest recovery to 366 in 2025 suggests stabilization around a sustainable baseline, with scholars analyzing underlying technology (provenance, digital ownership) rather than speculative marketplaces.

- Research Trajectory Analysis, 128,286-paper corpus"DeFi research grew 74x from 2019 to 2025 with no sign of deceleration. NFT research peaked in 2023 and is declining. Academic interest follows demonstrated utility, not market speculation."

V. Post-Quantum Urgency

The fastest-rising keywords in the corpus are dominated by quantum-resistance research. "Quantum resistant" grew 6.6x (from 37 to 243 papers) and "post-quantum" grew 3.9x (95 to 367 papers) between the 2022 to 2023 and 2025 to 2026 periods. Together they account for 610 papers in 2025 to 2026. This is a research community preparing for a potential existential threat to existing blockchain systems.

The urgency is real. Most blockchain systems rely on elliptic curve cryptography (ECDSA for Bitcoin and Ethereum) that is theoretically vulnerable to Shor's algorithm on a sufficiently powerful quantum computer. The NIST post-quantum cryptography standardization in 2024 (selecting CRYSTALS-Kyber and CRYSTALS-Dilithium as standard algorithms) has accelerated academic work on quantum-safe blockchain designs.

The full momentum map across all rising research themes is below.

Topic Momentum Dashboard (2025-2026 vs. 2022-2023)

Analyzing relative research velocity against absolute document countsFour categories structure the fastest-rising terms.

- Post-Quantum Security. "Quantum resistant" (6.6x) and "post-quantum" (3.9x), totaling 610 combined papers preparing blockchain for the quantum threat.

- Scalability Infrastructure. "Layer 2" (4.2x), "zk rollup" (3.4x), and "cross chain" (2.0x). Active engineering on rollups, state channels, and interoperability bridges.

- Institutional Adoption. "Regulatory" (3.5x, 4,529 papers), "real world asset" (5.6x), and "stablecoin" (2.7x). Research focused on institutional finance, not experimental protocols.

- Core DeFi. "DeFi" (2.6x), "decentralized finance" (2.0x), and "interoperability" (2.2x). Sustained growth as protocols mature and cross-chain infrastructure develops.

Declining terms confirm the pattern. "NFT" declined to 0.8x and "metaverse" to 0.8x. Both experienced hype-driven peaks and are now in structural contraction.

VI. The Global Research Map

China and India have reached near-parity at the top of global blockchain research output, a finding that contrasts with most other computer science fields where China leads by a wider margin.

China leads with 17,258 papers (13.5%), followed by India at 17,037 (13.3%) and the United States at 12,488 (9.7%). The top three countries account for 36.5% of all papers. The US ranking of third is notable. In most computer science research rankings, the US holds first or second position. Regulatory uncertainty around cryptocurrency may have dampened American academic engagement.

Emerging research economies contribute significantly. Indonesia (3,106 papers, rank 6) reflects Southeast Asia's high cryptocurrency adoption rate. Saudi Arabia (2,423, rank 10) signals Gulf states' strategic investment in blockchain and fintech infrastructure. No single US institution appears in the top eight institutional rankings. American blockchain research is distributed across many institutions rather than concentrated in a few.

VII. The Citation Economy

The citation distribution across 128,286 blockchain papers follows an extreme power law. 43.5% of all papers have received zero citations. The high zero-citation rate is partially explained by the recency of the corpus. 82.7% of papers were published from 2020 onward and have had limited time to accumulate citations.

Corpus Citation Skewness Distribution

Exploration of academic citations and citation inequalityPareto curve colored relative to active slider. As you slide from 50th (median) to 99th percentile, notice how the citation thresholds grow exponentially.

Distribution Segment Selector

Threshold Cutoff

42 citations

A paper in the 95th percentile of the corpus requires at least 42 citations.

Fewer than 0.1% of papers have 1,000+ citations, yet they account for a disproportionate share of the field's total citation volume.

VIII. Strategic Implications

The aggregation of 128,286 research papers yields three strategic imperatives for technology leaders, policymakers, and institutional investors.

-

Quantum-Proof Your Blockchain Strategy. Now. Post-quantum cryptography is the fastest-rising research theme in the corpus (6.6x growth). The NIST standardization of quantum-resistant algorithms in 2024 has shifted the question from "if" to "when." Organizations running blockchain infrastructure on elliptic curve cryptography face an existential migration challenge. Begin evaluating lattice-based signature schemes and hybrid cryptographic approaches today.

-

Follow the Research, Not the Hype. The DeFi-NFT divergence demonstrates that academic attention tracks demonstrated utility with remarkable precision. DeFi research accelerates (74x growth) because it solves a persistent structural problem. NFT research declines because the speculative use case collapsed. Capital allocation should weight research momentum (terms growing at 2x+) over market narratives. The data shows that regulatory infrastructure (3.5x), layer-2 scaling (4.2x), and real-world asset tokenization (5.6x) are the sectors commanding sustained intellectual capital.

-

Recognize the Geographic Shift. China and India together produce 26.8% of all blockchain research, more than double the US contribution. The institutional concentration is equally telling. The Chinese Academy of Sciences alone produces 924 papers, and Indian technical institutes occupy two of the top six global positions. Western organizations cannot assume leadership in blockchain standards, protocols, or regulatory frameworks without actively engaging the research communities driving the highest-volume output.

The underlying bibliometric dataset and methodology are detailed in the companion research paper "Blockchain Research Trends - A Bibliometric Analysis of 128,286 Papers (2013 to 2026)." The empirical corpus is available in the Web3 Reports Library.